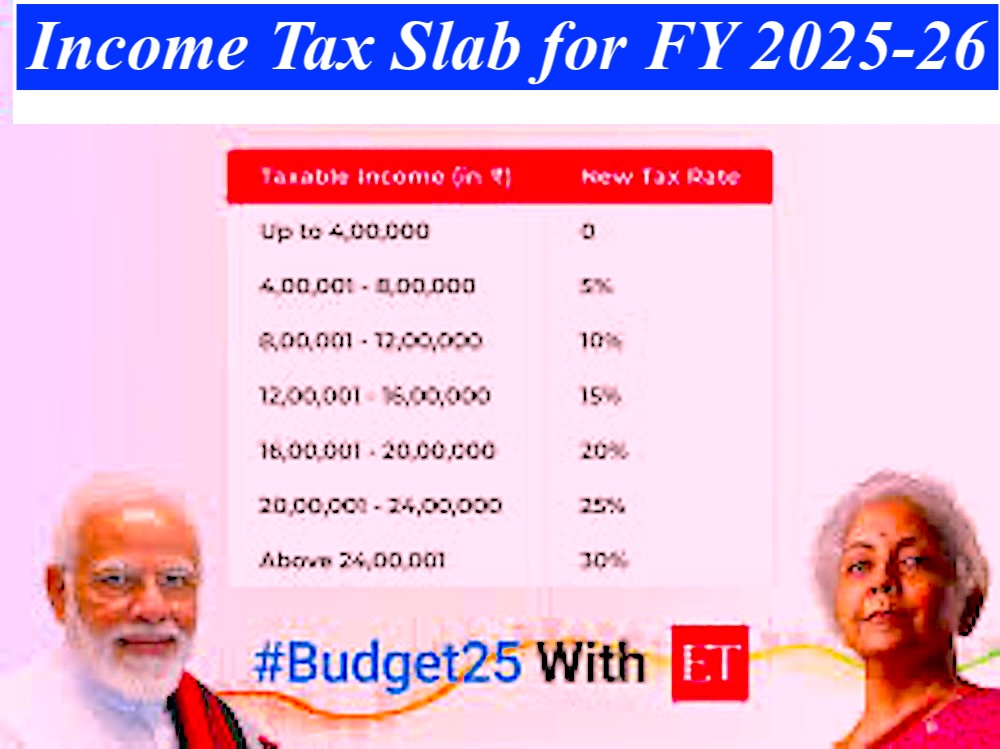

income tax slabs under the new tax regime in Union Budget 2025. The new income tax slabs under the new tax regime will come into effect from April 1, 2025 for the upcoming financial year 2025-26. The income tax slabs under the new tax regime have completely changed. The proposed income tax slabs under the new tax regime for FY 2025-26 are as follows: Rs 0- Rs 4 lakh Nil tax, Rs 4 lakh and Rs 8 lakh – 5%, Rs 8 lakh and Rs 12 lakh – 10%, Rs 12 lakh and Rs 16 lakh – 15%, Rs 16 lakh and Rs 20 lakh – 20%, Rs 20 lakh and Rs 24 lakh – 25% and above Rs 24 lakh – 30%. The new income tax slabs under new tax regime will allow taxpayers to save up to Rs 1.14 lakh in a financial year. The new tax regime continues to remain the default tax regime.

Income Tax Slab for FY 2025-26

Apart from making income tax changes, the tax rebate under Section 87A has been proposed to be hiked to Rs 60,000. The proposed hike in tax rebate under Section 87A will ensure that there is zero tax payable on incomes up to Rs 12 lakh. Current income tax laws allow zero tax on net taxable incomes up to Rs 7 lakh. This makes them eligible for current tax rebate of up to Rs 25,000.

The new income tax slabs proposed under new tax regime have hiked the income tax basic exemption limit to Rs 4 lakh from current limit of Rs 3 lakh.

No changes have been proposed in the deductions available under the new tax regime. For the upcoming fiscal year 2025-26, the individual will continue to claim standard deduction of Rs 75,000 from salary income and 14% of basic salary as employer’s contribution to the NPS Tier-I account.

There is no change in the surcharge levied on the income tax liability under the new tax regime for FY 2025-26.

The proposed changes in the new tax regime will make it more attractive for the taxpayers. It is likely that more taxpayers will now opt for the new tax regime going forward.

Announced in the old tax regime

No major changes have been announced in the old tax regime. However, parents investing in NPS Vatsalya for their children will soon be eligible for deduction under Section 80CCD (1b) of the Income Tax Act. This deduction will be available over and above Rs 1.5 lakh available under Section 80C. This deduction is available for additional investment made in NPS for up to Rs 50,000 under the old tax regime. Further, tax rebate of Rs 12,500 will continue to be available under the old tax regime if the taxable incomes do not exceed Rs 5 lakh.

The main difference between the old and new tax regime is the availability of usual deductions and tax exemptions. The new tax regime does not allow deduction of common deductions such as Section 80C deduction up to Rs 1.5 lakh for specified investments and expenditures, Section 80D deduction up to Rs 25,000/Rs 50,000 for health insurance premium paid and Section 80TTA deduction of up to Rs 10,000 for interest earned from savings accounts of bank and post office, among others.

income tax slabs applicable

The income tax slabs applicable under the old tax regime depends on the age of individual. The old tax regime offered multiple basic income exemption limits depending on the age of the taxpayer. For individuals below 60 years of age, the basic income exemption limit is Rs 2.5 lakh. For senior citizens aged 60 years and above but below 80 years, the basic exemption limit is Rs 3 lakh. For super senior citizens aged 80 years and above, the basic exemption limit is Rs 5 lakh.

Proposed Income Tax Slabs for FY 2025-26 (AY 2026-27) under New Tax Regime:

- Rs 0 to Rs 4,00,000 – Nil

- Rs 4,00,001 to Rs 8,00,000 – 5%

- Rs 8,00,001 to Rs 12,00,000 – 10%

- Rs 12,00,001 to Rs 16,00,000 – 15%

- Rs 16,00,001 to Rs 20,00,000 – 20%

- Rs 20,00,001 to Rs 24,00,000 – 25%

- Above Rs 24,00,000 – 30%

income tax Key Highlights:

- Tax Rebate under Section 87A: The rebate has been increased to Rs 60,000, ensuring that taxpayers with incomes up to Rs 12 lakh pay no income tax.

- Basic Exemption Limit: Increased to Rs 4 lakh (from Rs 3 lakh) under the new tax regime.

- Standard Deduction: A standard deduction of Rs 75,000 remains available for salaried individuals.

- Employer’s NPS Contribution: The contribution to NPS Tier-I continues to be eligible for a tax deduction of 14% of basic salary.

Tax Calculation Example for FY 2024-25 under the New Tax Regime:

For a gross total income of Rs 20 lakh and eligible deductions (standard deduction of Rs 75,000 and NPS contribution of Rs 2 lakh):

- Net Taxable Income: Rs 20,00,000 – Rs 75,000 – Rs 2,00,000 = Rs 17,25,000

- Tax Breakdown:

- 0 to Rs 4 lakh: No tax

- Rs 4,00,001 to Rs 7,00,000 (Rs 3 lakh) at 5% = Rs 15,000

- Rs 7,00,001 to Rs 10,00,000 (Rs 3 lakh) at 10% = Rs 30,000

- Rs 10,00,001 to Rs 12,00,000 (Rs 2 lakh) at 15% = Rs 30,000

- Rs 12,00,001 to Rs 15,00,000 (Rs 3 lakh) at 20% = Rs 60,000

- Above Rs 15,00,000 (Rs 2,25,000) at 30% = Rs 67,500

- Total Tax: Rs 2,07,500

- Cess at 4%: Rs 8,300

- Final Tax Payable: Rs 2,15,800

Old Tax Regime Slabs (FY 2024-25) for Comparison:

- Up to Rs 2.5 lakh – Nil

- Rs 2.5 lakh to Rs 5 lakh – 5%

- Rs 5 lakh to Rs 10 lakh – 20%

- Above Rs 10 lakh – 30%

Additionally, there are deductions like Section 80C (up to Rs 1.5 lakh), 80D (medical insurance), and 80TTA (savings interest), which are available in the old tax regime but not in the new tax regime.

Taxpayer Choice Between Regimes:

- New Tax Regime: Simpler and more attractive for taxpayers with fewer deductions but offers lower tax rates.

- Old Tax Regime: Beneficial for those who have significant deductions, exemptions, and tax-saving investments.

Changes in the Old Tax Regime:

- NPS Vatsalya: Parents investing in NPS for their children can claim an additional deduction of up to Rs 50,000 for investment in NPS.

- Tax Rebate: For taxpayers earning below Rs 5 lakh, a tax rebate of Rs 12,500 remains available.

Important Notes:

- Surcharge: Remains unchanged, and it will apply if the total income exceeds Rs 2 crore at 25%.

- Cess: A 4% cess on the total tax payable is applicable across both tax regimes.

How to calculate income tax payable under new tax regime

|

Particulars |

Amount (In Rs) |

|

Gross total income |

20,00,000 |

|

Standard deduction from salary/pension |

(75,000) |

|

Deduction under section 80CCD (2) |

(2,00,000) |

|

Net taxable income |

17,25,000 |

|

Hence, the net taxable income on which income tax payable is to be calculated will be Rs 17.25 lakh (Rs 20 lakh minus Rs 2.75 lakh). |

|

Under the new income tax regime, income between 0 to Rs 3 lakh is exempted from tax. Hence, no tax will be payable on this income. After deducting income of Rs 3 lakh from Rs 17.25 lakh the income left which is still chargeable to tax is Rs 14.25 lakh. |

|

The next income tax slab is Rs 3,00,001 and Rs 7,00,000. Thus, out of taxable income of Rs 14.25 lakh, Rs 4 lakh (Rs 7 lakh minus Rs 3 lakh) will be taxed at 5%. The tax payable here will be Rs 20,000. After this, the income left to be taxed is Rs 10.25 lakh (Rs 14.25 lakh minus Rs 4 lakh). |

|

The next income tax slab is Rs 7,00,001 and Rs 10,00,000. Out of taxable income of Rs 10.25 lakh, the taxable income of Rs 3 lakh (Rs 10 lakh minus Rs 7 lakh) will be taxed at 10%. The tax payable here will be Rs 30,000. After this, the income left to be taxed will be Rs 7.25 lakh. |

|

The next income tax slab is Rs 10,00,001 and Rs 12,00,000. Out of the balance income of Rs 7.25 lakh, Rs 2 lakh will be taxed at 15%. The tax payable under this slab will be Rs 30,000. After this income left for chargeable under the tax will be Rs 5.25 lakh. |

|

The next income tax slab is Rs 12,00,001 and Rs 15,00,000. Here out of the taxable income of Rs 5.25 lakh, Rs 3 lakh (Rs 15 lakh minus Rs 12 lakh) will be taxed at 20%. The tax payable amount here will be Rs 60,000. After this, the income left to be taxed is Rs 2.25 lakh. |

|

The final income tax slab is for incomes above Rs 15 lakh. The balance taxable income of Rs 2.25 lakh will be taxed at 30%. The tax payable here will be Rs 67,500. |

|

The total tax payable by an individual will be Rs 2,07,500. In this tax amount, the cess at 4% will be added to this amount for final tax amount payable. |

Income (Rs) and Tax amount (Rs)

|

Particulars |

Income (Rs) |

Tax amount (Rs) |

|

Net taxable income |

17,25,000 |

– |

|

Income exempt up to Rs 3 lakh |

(3,00,000) |

0 |

|

Income which is still chargeable to tax (Rs 17.25 lakh – 3 lakh) |

14,25,000 |

– |

|

Income tax slab of Rs 3 lakh and up to Rs 7 lakh |

(4,00,000) |

@ 5% = 20,000 |

|

Income which is still chargeable to tax (Rs 14.25 lakh – 4 lakh) |

10,25,000 |

– |

|

Income tax slab of Rs 7 lakh up to Rs 10 lakh |

(3,00,000) |

@ 10% = 30,000 |

|

Income which is still chargeable to tax (Rs 10.25 lakh -3 lakh) |

7,25,000 |

– |

|

Income tax slab of Rs 10 lakh up to Rs 12 lakh |

(2,00,000) |

@15% = 30,000 |

|

Income which is still chargeable to tax (Rs 7.25 lakh – 2 lakh) |

5,25,000 |

– |

|

Income tax slab of Rs 12 lakh up to Rs 15 lakh |

(3,00,000) |

@ 20% = 60,000 |

|

Income which is still chargeable to tax (Rs 5.25 lakh-3 lakh) |

2,25,000 |

– |

|

Income tax slab of above Rs 15 lakh |

(2,25,000) |

@30% = 67,500 |

|

Total income tax liability |

– |

2,07,500 |

|

Cess at 4% on total income tax payable (i.e. on Rs 2,07,500) |

– |

8,300 |

|

Final income tax liability (inclusive of cess) |

– |

2,15,800 |

|

The final tax payable on gross income of Rs 20 lakh is Rs 2,15,800, after claiming deductions of Rs 2.75 lakh. The surcharge is also applicable if the income is above Rs 50 lakh. |

How to calculate income tax liability under old tax regime

|

Particulars |

Amount (in Rs) |

|

Gross total income |

17,00,000 |

|

Section 80C |

(1,50,000) |

|

Section 80 CCD(1b) NPS investment |

(50,000) |

|

Section 80D – medical insurance premium |

(25,000) |

|

Section 80TTA |

(10,000) |

|

Net taxable income |

14,65,000 |

After deducting the deductions from the gross total income, one arrives at the net taxable income of Rs 14,65,000. The tax payable will be calculated on the net taxable income.

As per the income tax slab rates table, the first Rs 2.5 lakh from net taxable income will be exempted from tax. This is because there is no tax on income up to Rs 2.5 lakh as per current income tax slabs in the old tax regime. Post this, income left on which tax has to be calculated is Rs 12,15,000 (14,65,000-2,50,000). The second slab in the income tax slab table is Rs 2.5 lakh and Rs 5 lakh which is taxed at Rs 5%. This means that out of Rs 12,15,000, then next Rs 2,50,000 will be taxed at 5%. The tax amount will be Rs 12,500.

Now the income left which is still chargeable to tax is Rs 9,65,000. The third slab in the income tax slab table is Rs 5 lakh and Rs 10 lakh, taxed at 20%. This means that out Rs 9,65,000, Rs 5,00,000 will be taxed at 20%. The tax payable here will be Rs 1,00,000.

The balance income on which tax has to be calculated is Rs 4,65,000. The tax amount on this balance income (Rs 14,65,000 minus Rs 10,00,000) will be calculated on the basis of the last slab, i.e., above Rs 10 lakh at the rate of 30%. The tax payable amount comes out to be Rs 1,39,500.

Hence, the total tax payable by an individual will be Rs 2,52,000 (Rs 12,500 + 1,00,000+ 1,39,500).

|

Particulars |

Income (Rs) |

Tax amount (Rs) |

|

Net taxable income |

14,65,000 |

– |

|

Income exempt up to Rs 2,50,000 |

(2,50,000) |

0 |

|

Income which is still chargeable to tax (Rs 14,65,000 – 2,50,000) |

12,15,000 |

– |

|

Income tax slab of Rs 2.5 lakh and up to Rs 5 lakh |

(2,50,000) |

@ 5% =12,500 |

|

Income which is still chargeable to tax (Rs 12,15,000 – 2,50,000) |

9,65,000 |

– |

|

Income tax slab of Rs 5 lakh up to Rs 10 lakh |

(5,00,000) |

@20% = 1,00,000 |

|

Income which is still chargeable to tax (Rs 9,65,000 – 5,00,000) |

4,65,000 |

– |

|

Income tax slab of above Rs 10 lakh |

(4,65,000) |

@ 30% =1,39,500 |

|

Total income tax liability |

– |

2,52,000 |

|

Cess at 4% on total income tax payable (i.e. on Rs 2,52,000) |

– |

10,080 |

|

Final income tax liability (inclusive of cess) |

– |

2,62,080 |

How to know which income tax slab you fall in

For example, your gross total income from all sources is Rs 12 lakh and you are eligible to claim deduction of Rs 2.10 lakh under sections 80C, 80TTA, 80CCD(1b). The taxable income on which you have to calculate tax will be Rs 9.9 lakh (Rs 12 lakh – Rs 2.10 lakh). Your income tax slab in the old tax regime will be between Rs 5 lakh and Rs 10 lakh. The tax rate is the 20%.

However, the income tax slabs and income tax rules under the new tax regime have been revised in the July budget 2024. From April 1, 2024, the new tax regime allows standard deduction of Rs 75,000 from salary and pension income and Section 80CCD (2) deduction up to 14% on basic salary for employer’s contribution to the employee’s Tier-I NPS account.

From the example above, after claiming deduction, the taxable income is, say, Rs 9.9 lakh (Gross taxable income of Rs 12 lakh minus Rs 2.10 lakh). The net taxable income of Rs 9.9 lakh falls under the revised income tax slab of Rs 7,00,001 and Rs 10,00,000. This will be taxed at 10%.

Surcharge on income tax

The July budget 2024 has not made any changes in the surcharge rates applicable on the income tax amounts under the new and old tax regimes. If an individual’s net taxable income exceeds a specified level, then a surcharge is levied. The surcharge is levied on the income tax payable amount before the levy of cess. According to income tax laws, a surcharge is applicable if an individual’s taxable income exceeds Rs 50 lakh.

From FY 2023-24, the government made changes in the surcharge rates under the new tax regime. The new surcharge rates have come into effect from April 1, 2023.

|

Surcharge rate from April 1, 2023 under new tax regime |

|

|

Income range |

Surcharge rate |

|

Up to Rs 50 lakh |

Nil |

|

More than Rs 50 lakh but up to Rs 1 crore |

10% |

|

More than Rs 1 crore but up to Rs 2 crore |

15% |

|

More than Rs 2 crore |

25% |

However, individuals opting for the old tax regime in current FY 2024-25 will continue to pay the surcharge rate they were paying in the previous financial years.

Surcharge rate under old tax regime

|

Surcharge rate under old tax regime |

|

|

Income range |

Surcharge rate |

|

Upto Rs 50 lakh |

Nil |

|

More than Rs 50 lakh but up to Rs 1 crore |

10% |

|

More than Rs 1 crore but up to Rs 2 crore |

15% |

|

More than Rs 2 crore but up to Rs 5 crore |

25% |

|

More than Rs 5 crore |

37% |